When you pick up a generic prescription at the pharmacy, you might think the price is simple: a few dollars, maybe less than a coffee. But behind that low cost is a web of laws, contracts, and reimbursement rules that determine exactly how much the pharmacy gets paid-and whether it can even stay open. These aren’t just background details. They directly affect whether you get your meds, how much you pay out of pocket, and even if your local pharmacist can afford to keep the lights on.

How Generic Drugs Got Their Price Tag

The modern system for paying pharmacies for generic drugs started with the Hatch-Waxman Act of 1984. This law created a fast-track path for generic drug makers to get FDA approval without repeating expensive clinical trials. The goal? Bring down drug prices by letting multiple companies make the same medicine. And it worked. Today, generics make up 90% of all prescriptions filled in the U.S., but only 23% of total drug spending. That’s billions in savings every year.But here’s the catch: just because a generic drug is cheaper doesn’t mean the pharmacy gets paid enough to cover its costs. Reimbursement isn’t based on what the pharmacy actually paid for the pills. Instead, it’s based on outdated benchmarks like Average Wholesale Price (AWP) or, more commonly now, Maximum Allowable Cost (MAC) lists.

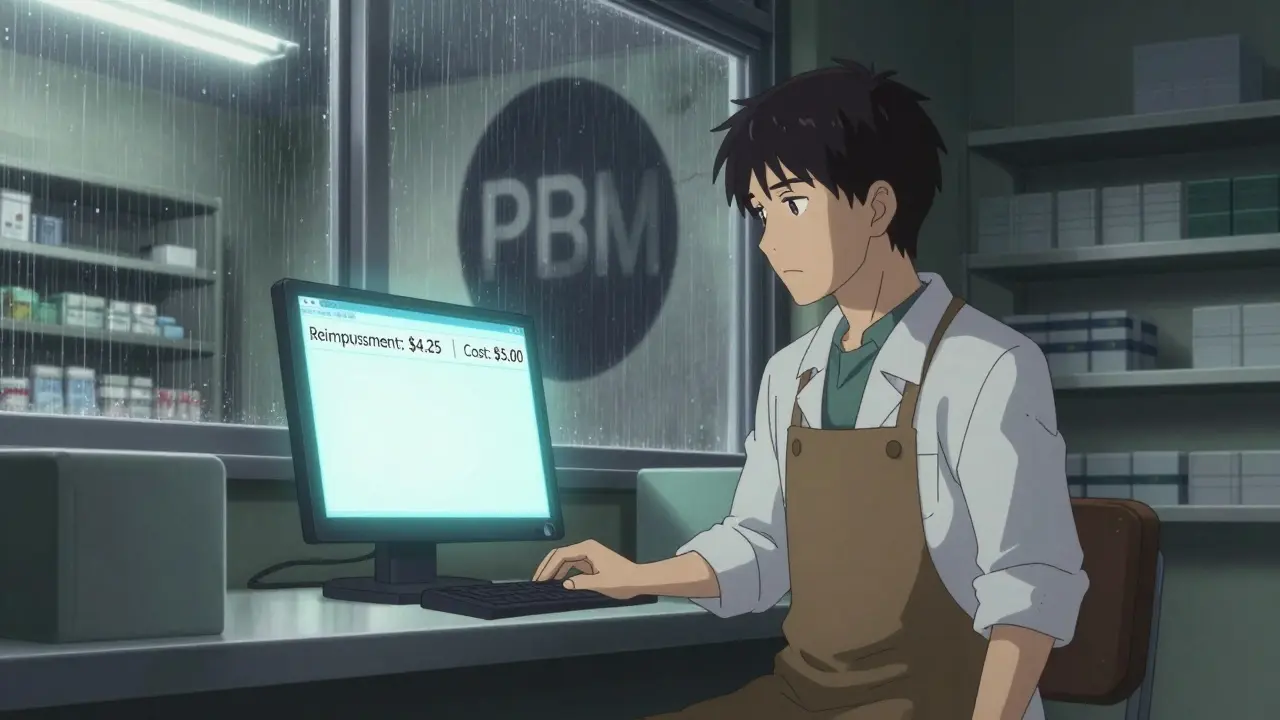

MAC lists are set by pharmacy benefit managers (PBMs) and reflect what they think a generic drug should cost. If the pharmacy bought the drug for $5 but the MAC is $4.25, the pharmacy loses 75 cents per prescription. No one tells them this ahead of time. They just get paid less than they paid.

Who’s Really in Charge: PBMs and Their Hidden Fees

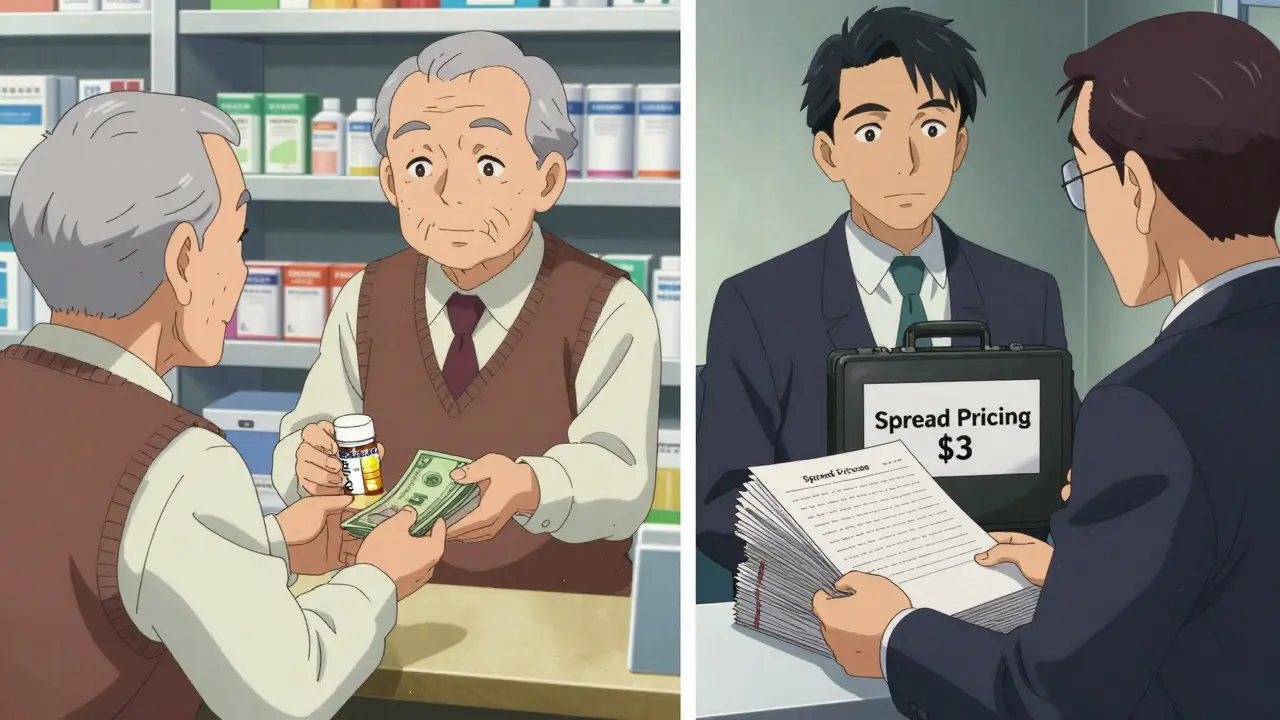

Pharmacy Benefit Managers (PBMs) like CVS Caremark, Express Scripts, and OptumRX control nearly 80% of all prescription claims in the U.S. They’re hired by insurance companies and Medicare Part D plans to manage drug coverage. But their business model isn’t transparent.One major source of their profit is called spread pricing. Here’s how it works: Your insurer agrees to pay $10 for a generic drug. The PBM tells the pharmacy it will be paid $7. The PBM pockets the $3 difference. That’s the spread. And until 2018, many PBMs had gag clauses in their contracts-preventing pharmacists from telling you that paying cash might be cheaper than using your insurance.

These practices hit small pharmacies hardest. In 2023, the average margin on generic drugs was just 1.4%. In 2018, it was 3.2%. That’s not enough to cover rent, staff wages, or even rising fuel costs for deliveries. Many independent pharmacies now operate on razor-thin margins, and some have closed.

Medicare Part D and the Patchwork of Rules

Medicare Part D covers 50.5 million Americans. It’s supposed to help seniors afford meds-but its reimbursement system is confusing. Each Part D plan has its own formulary, which determines which drugs are covered and at what cost-sharing level.Generics usually sit in lower tiers, meaning lower copays. But not always. Some plans still require prior authorization for generics, even when they’re cheaper than the brand. In 2022, 28% of Part D plans required prior authorization for at least one generic drug. That means extra paperwork, delays, and frustration for patients and pharmacists alike.

There’s also the donut hole-a coverage gap where you pay full price after hitting your initial coverage limit. While the Inflation Reduction Act of 2022 capped out-of-pocket spending at $2,000 starting in 2025, many seniors still face unpredictable costs. And for those without Extra Help, generic copays can vary wildly between plans. One plan might charge $4 for a generic; another might charge $12.

State Laws Are Trying to Fix the System

Frustrated by PBM practices, 44 states have passed laws to regulate how pharmacies are paid for generics. These include:- Prohibiting gag clauses (now federally banned, but some states had them earlier)

- Requiring PBMs to pay pharmacies at least their actual acquisition cost

- Setting minimum reimbursement rates for generic drugs

- Creating appeals processes for pharmacies denied reimbursement

For example, in California, PBMs must now disclose their reimbursement formulas. In Texas, pharmacies can sue if they’re paid less than their cost. These laws help, but they’re not uniform. A pharmacy in New York might get paid fairly, while one in Alabama gets crushed under the same PBM contract.

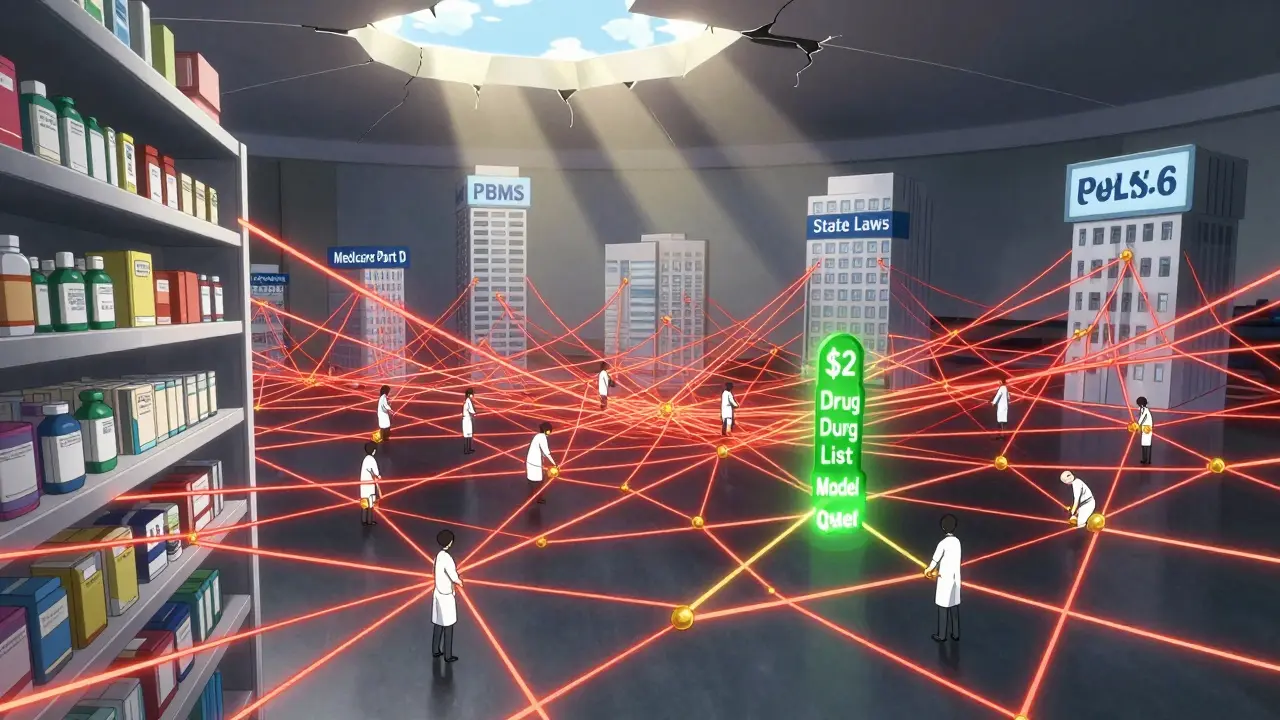

The $2 Drug List: A New Direction?

In 2025, the Centers for Medicare & Medicaid Services (CMS) is testing a bold new idea: the Medicare $2 Drug List Model. The concept is simple-take about 100 to 150 essential generic drugs and cap the patient copay at $2. No formularies. No tiers. No prior authorizations.It’s modeled after what big retailers like Walmart and Costco already do: fixed, low prices for common generics. But instead of being a retail perk, it would be built into Medicare Part D. The drugs selected are based on three things: how often they’re used, how important they are clinically, and whether multiple manufacturers make them (to avoid supply shortages).

If this works, it could be the biggest shift in generic reimbursement since Hatch-Waxman. It removes the middleman, cuts administrative clutter, and puts patients first. Early data from pilot programs show improved adherence and lower overall spending.

What This Means for You

If you take generics regularly, here’s what you should know:- Ask your pharmacist: “Is this cheaper if I pay cash?” Even with insurance, cash prices are often lower.

- Check if your Part D plan has a preferred generic tier. If not, consider switching plans during open enrollment.

- Use mail-order pharmacies or retail chains like Walmart or Kroger-they often have $4 generic lists that beat insurance copays.

- If you’re denied coverage for a generic, file an appeal. Many denials are overturned.

Pharmacists aren’t just dispensing pills. They’re navigating a broken system designed to save money-but often at their expense. The laws around reimbursement aren’t just about dollars and cents. They’re about whether people can afford to stay healthy.

What’s Next?

The pressure is mounting. Generic drug prices are still falling-about 5-7% per year-but reimbursement rates haven’t kept up. PBMs are under scrutiny from the FTC, which is cracking down on “pay-for-delay” deals that block generics from entering the market. Meanwhile, state laws are tightening, and CMS is testing bold alternatives.The real question isn’t whether generics save money. They do. The question is: who gets to keep those savings? Right now, the answer is often the middlemen-not the patients, not the pharmacies, and not the manufacturers who make the drugs affordable in the first place.

11 Comments

Jessica Chaloux

4 March, 2026I just cried reading this. 😭 My grandma’s blood pressure med went from $4 to $12 last year. She’s on a fixed income. I didn’t even know pharmacies were losing money. This isn’t just about drugs-it’s about people.

Mariah Carle

5 March, 2026The system is designed to make you feel grateful for scraps. 🤔 We’ve normalized exploitation as ‘efficiency.’ PBMs aren’t intermediaries-they’re rent-seekers in white coats. The real innovation? Removing them entirely. The $2 list isn’t a fix-it’s a return to sanity.

Pankaj Gupta

5 March, 2026This is one of the clearest explanations I’ve read on pharmacy economics. The disconnect between acquisition cost and reimbursement is staggering. It’s not just unfair-it’s economically irrational. States that mandate payment above cost are doing the bare minimum. The federal government should standardize this.

Richard Elric5111

7 March, 2026The structural inefficiencies inherent in the current pharmaceutical reimbursement paradigm are a direct consequence of regulatory capture and the commodification of healthcare. The Hatch-Waxman Act, while laudable in intent, inadvertently enabled the rise of oligopolistic intermediaries who extract value without generating commensurate utility. A systemic recalibration is not merely advisable-it is ontologically necessary.

Dean Jones

8 March, 2026Let me tell you something. I worked in a small-town pharmacy for five years. We had a guy who came in every week for his diabetes meds. He’d hand over his insurance card and then pay $18 cash because the copay was $22. We’d lose 60 cents per script. We had to cut staff. We had to close on Sundays. The PBM didn’t care. The insurer didn’t care. The government didn’t care. The only people who cared were the ones who showed up with the cash in hand and the fear in their eyes. This isn’t policy. This is cruelty dressed up as a balance sheet.

Betsy Silverman

9 March, 2026I’ve been a pharmacist for 18 years. I’ve seen this happen. The $2 list could be revolutionary-if it’s implemented right. But we need to make sure it doesn’t get gamed. PBMs will find a way to sneak fees back in. We need transparency laws that actually stick. And we need to stop treating pharmacists like clerks. We’re the last line of defense against people not taking their meds.

Ivan Viktor

10 March, 2026So let me get this straight. The system is so broken that the only way to get cheap meds is to go to Walmart? Cool. So we’ve outsourced healthcare to big-box stores because the ‘experts’ failed. I’m just glad my dog’s heart medication is cheaper than my phone bill.

Zacharia Reda

12 March, 2026You know what’s wild? The fact that we’re even having this conversation. Imagine if we treated antibiotics like we treat toilet paper-just put them on the shelf at a flat price and let people grab them. No forms. No approvals. No middlemen. The $2 list is basically that. Why is this radical? Because we’ve let profit dictate health.

Mike Dubes

13 March, 2026omg this is so real. my mom got her blood pressure med for $4 at walmart but her insurance said it was $15. she was so confused. i told her to always ask the pharmacist. they know. they see it every day. also-did you know some places will give you 90-day supplies for like $10? just ask. they want you to get better, not broke. ❤️

Helen Brown

15 March, 2026This is all a cover-up. PBMs are working with the government to control what drugs you get. They’re poisoning the system so you’ll need more meds. They don’t want you healthy. They want you dependent. Look at the numbers. It’s all connected. Someone’s watching. Always.

marjorie arsenault

16 March, 2026To everyone who’s feeling overwhelmed: you’re not alone. Talk to your pharmacist. Ask for help. Use mail-order. Switch plans. You have more power than you think. And if you’re a student, a parent, a grandkid-speak up. This isn’t just about money. It’s about dignity. We can fix this. One conversation at a time.